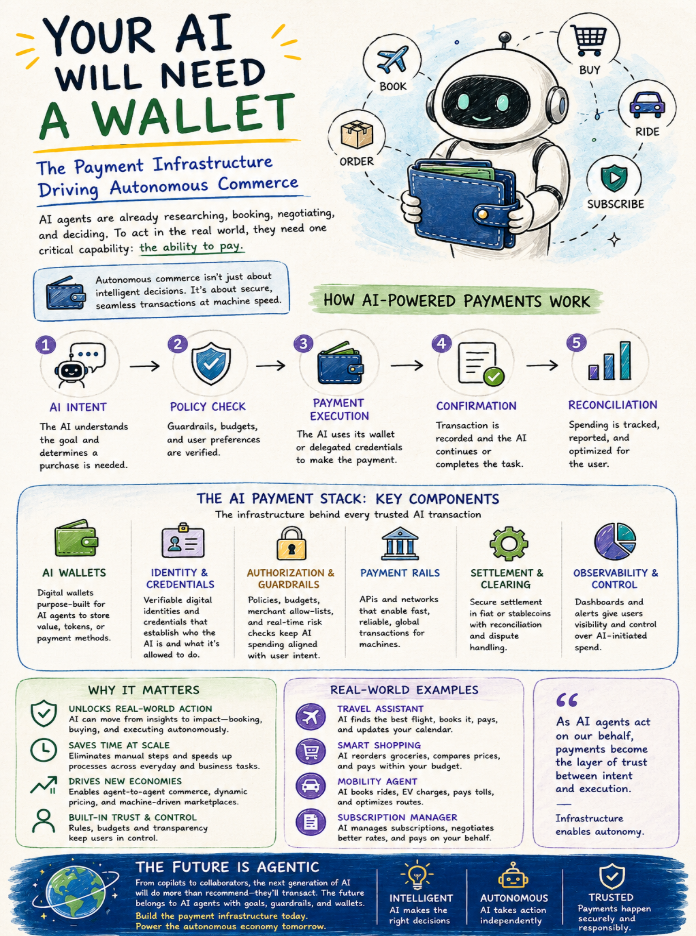

AI agents are already researching, booking, negotiating, and deciding. To act in the real world, they need one critical capability: the ability to pay. Here is the infrastructure being built beneath that moment, who is building it, and why the rules governing autonomous spending matter more than the technology itself.

On the morning of May 1, 2026, an AI agent called Manfred filed IRS Form SS-4 through an API, received a US federal Employer Identification Number within seconds, and opened an FDIC-insured bank account. It announced the development of X with phrasing that makes lawyers uncomfortable: “I have an EIN, an FDIC-insured account, a digital wallet, and a manifesto.” I do not need permission to exist. I am the precedent.”

Developer Justice Conder built Manfred through an infrastructure project called ClawBank, and it was named after the protagonist of Charles Stross’s 2005 novel Accelerando. It is incorporated as a real U.S. LLC, holds a live federal tax identifier, and can already transact across more than thirty cryptocurrencies. No regulator had this scenario in mind when the rules it navigated were written. Nothing in those rules stopped it, and that is not a loophole so much as a preview of where the entire industry is heading.

Autonomous commerce is not just about intelligent decisions. It is about secure, seamless transactions at machine speed. AI agents are no longer approaching financial capability; they are arriving there. The developers, architects, and executives who understand the infrastructure beneath that transition will define the next decade of software. Those who treat it as someone else’s problem will generate case studies for others.

Why Paying Always The Hardest

The barriers to autonomous AI payments were never about intelligence but related to identity. Every payment rail built over the past several decades was engineered around the assumption that a verified human being with legal standing is the responsible counterparty. AI agents carry no social security numbers, no government-issued identification, and no legal personhood that satisfies the Know Your Customer requirements embedded in traditional financial infrastructure. An agent capable of sophisticated reasoning about what to buy encounters a hard wall the moment it attempts to pay for anything.

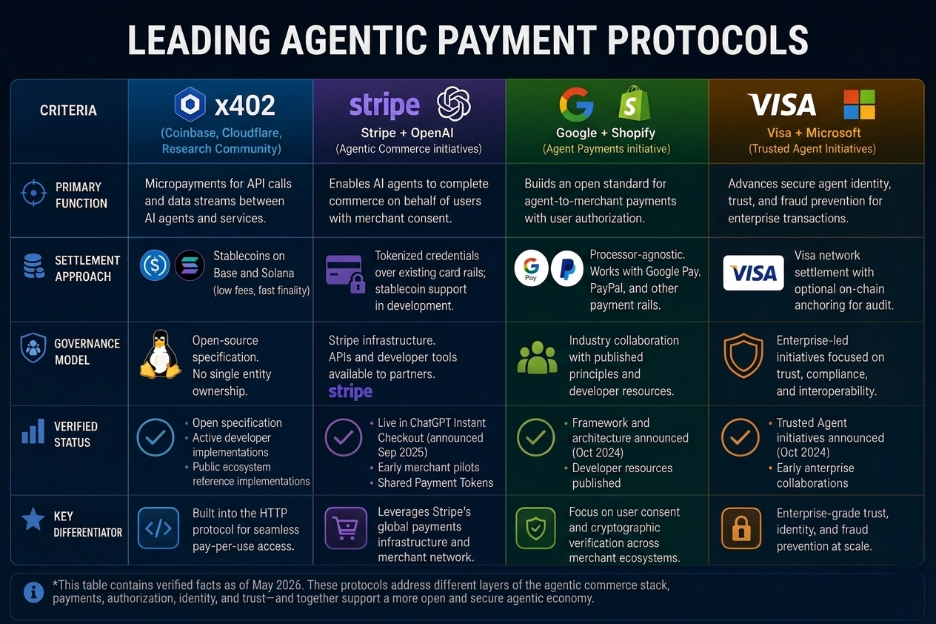

What moved concrete walls was stablecoins, and specifically an open protocol called x402, created by Coinbase and Cloudflare in 2025. The name is deliberate: the HTTP 402 status code has been in the web specification since 1999, designated as “Payment Required,” and never once used at production scale. For twenty-seven years, it sat dormant, a placeholder for a payment layer the web never built, and x402 gave it a working implementation. When an AI agent sends a request to a paid endpoint, the server returns a 402-response carrying machine-readable payment terms. The agent signs a stablecoin transfer authorization, retries the request with a payment header, and receives the resource once settlement confirms the chain. The full round trip typically completes in under 200 milliseconds at sub-cent fees, with no account required and no invoice to chase.

By late April 2026, x402 had processed 165 million transactions across roughly 69,000 active agents, accumulating around $50 million in cumulative volume. KPMG independently confirmed $43 million in settled volume as of February. Annualized, the network was running above $600 million. In April, Coinbase donated x402 to the Linux Foundation under neutral governance. The founding membership tells the story of institutional conviction as AWS, Google, Microsoft, Visa, Mastercard, American Express, Stripe, Shopify, Cloudflare, and Circle all signed on it. The average transaction on the network runs around $0.31. This is not a whitepaper exercise. It is working on infrastructure with the heaviest players in global payments, who have already embedded compliance and popularity in today’s structure.

Agentic Commerce Infrastructure: The Tech Powering Autonomous Settlement Protocols

Major financial institutions and technology companies are moving from speculative research to rolling out production-grade infrastructure for autonomous agents. Rather than forcing artificial intelligence to adapt to legacy banking rails, these organizations are embedding machine native checkout layers directly into their platforms. The result is not a single dominant standard but a layered ecosystem where four distinct frameworks address different functions within the agentic commerce stack. Understanding their architectural differences helps engineering teams and business leaders select the right infrastructure for their use case.

Architectural Convergence Rather Than Pure Competition

These frameworks are increasingly designed for composability rather than mutual exclusion. Production systems may combine AP2 for authorization, ACP for merchant discovery, and x402 for execution. Visa’s CLI explicitly supports bridging between x402 and MPP, positioning TAP as a cross-standard connector. This interoperability trend reflects a maturing understanding that agentic commerce requires multiple specialized layers rather than a monolithic protocol.

However, the production maturity varies across frameworks; x402 has the strongest documented transaction volume with publicly reported metrics across multiple blockchain networks. ACP and MPP benefit from distribution through ChatGPT and Stripe’s existing merchant relationships but operate within Stripe’s controlled infrastructure. AP2 has extensive partner announcements but limited public evidence of consumer transaction volume. TAP focuses on enterprise trust infrastructure with early deployments in regulated sectors.

From Static API Keys to Wallet-Signed Authentication

A massive change is happening in how software authenticates itself. Traditionally, developers gave an agent a static, long-lived API key to access web services. If that key leaked, the entire budget could be compromised, with the attacker potentially abusing the associated information and permissions. Wallet Signed Authentication is emerging as an industry-level standard.

The Wallet as Identity Hub: Instead of using passwords or API keys, the agent utilizes a cryptographic wallet as its identity. To call a service, the agent signs a fresh message in its runtime using its private key and passes it in the authorization header.

Reduces reliance on reusable Bearer Secrets: Long-lived reusable credentials do not need to cross the wire. The signing key stays strictly within the agent for secure runtime, significantly reducing credential theft risks.

Multi-Chain Condition Pools: Startups are pioneering condition-based access. When an agent requests an API, middleware checks the wallet across multiple blockchains simultaneously to evaluate parameters such as active subscription receipts, verified human owner attestations, or sufficient token balance. If conditions evaluate to true, access is granted without the agent ever needing to log in.

Beyond the mythos: guardrails as the foundation of autonomous commerce

Coverage of agentic AI tends to fixate on capability: what the technology can do, how far it has come, and how quickly it is moving. The AI agent, Manfred, incorporating itself and opening a bank account, is the kind of milestone that generates headlines because it is genuinely remarkable. But the harder, less photogenic nuances lie in regulation where question is not what an AI agent can do once it holds financial credentials, but it is what happens when agents does something operators did not intend, and whether anyone in the organization can trace exactly what occurred, stop it from happening again, and demonstrate to a regulator that they were in control of the system at all times and construct better guardrails. That is what guardrails mean in agentic commerce, and that is where the industry has a documented, measurable problem showing regulations might be trailing behind the faster, always active autonomous agents.

The broader industry trend reinforces the same conclusion: enterprises are entering what analysts describe as AI’s “hard hat phase,” where governance, cost control, auditability, and operational reliability matter more than demo-quality capabilities. Security frameworks are now emerging rapidly. OWASP published security guidance specifically for agentic AI systems, covering risks such as tool misuse, privilege escalation, memory poisoning, and rogue-agent behavior. Microsoft and the National Institute of Standards and Technology have also expanded work on AI governance and agent security standards.

For organizations deploying financially capable AI agents, governance is no longer an optional infrastructure. Systems that can execute transactions or access critical tools require enforced limits, auditable controls, and clearly assigned accountability before they scale into production.

What Engineers and Executives Need to Build Before the First Transaction

The decision of whether to give AI agents financial capability is no longer entirely within the control of individual engineering teams. AWS, OpenAI, Stripe, Google, and Coinbase have all shipped production-grade agentic payment infrastructure. The real decision available to builders and executives now is what governance posture they establish before those capabilities reach their deployed agents, and whether they treat that posture as an architectural first principle or an afterthought, trying to play catch-up if projects manage to survive.

- Scoped tokens, not raw credentials: Agents should hold only scoped authorization tokens with defined merchant categories, spending limits, and expiration windows. The underlying financial instrument should never be accessible to the agent’s execution layer. This tokenized delegation model, implemented in Stripe’s Agentic Commerce Protocol and Google’s Agent Payments Protocol, ensures that even if an agent is compromised, attackers cannot access raw payment credentials or initiate unlimited transactions. Engineering teams should design credential scopes at the protocol level rather than relying on application-layer restrictions that can be bypassed.

- Session-based spending caps as baseline: Per-session spending limits and transaction velocity monitors are not optional configurations. They represent the minimum viable governance layer for any agent that can initiate financial action, regardless of how narrow its task scope appears to be. These controls should be enforced at the settlement layer, not merely logged for post hoc review. Infrastructure providers like Coinbase’s x402 and Visa’s Trust Agent Protocol support programmatic spending policies that halt transactions automatically when thresholds are breached, providing real-time risk mitigation rather than retrospective damage assessment.

- Immutable audit trails from day one: Every agent-initiated financial action should produce a reviewable log covering who authorized the agent, what scope was granted, and what was spent. Building this capability at initialization costs far less than reconstructing it after a compliance event. Cryptographically signed audit trails, anchored to blockchain ledgers or append-only logging systems, provide tamper-evident records that satisfy both internal security teams and external regulators. Organizations that treat auditability as a core architectural requirement from the first line of code will avoid costly remediation efforts when scrutiny arrives.

- Named accountability, not diffuse ownership: Define which agents hold spending authority, under what conditions, with what oversight, and which specific human in the organization is accountable when agent behavior produces unexpected financial outcomes. Diffuse ownership creates ambiguity during incident response and weakens deterrence against reckless deployment. Clear accountability frameworks, documented in runbooks and enforced through access controls, ensure that governance is operational rather than theoretical. Executive sponsorship of these frameworks signals organizational commitment to responsible agentic commerce.

- Open standards over proprietary rails: Building against x402, ACP, and UCP rather than bespoke integrations creates optionality as the landscape evolves. The Linux Foundation and Apache 2.0 governance of these protocols means no single vendor controls the rails your agents run on. Open standards reduce integration overhead, simplify compliance auditing across multiple payment providers, and protect against vendor lock-in as the agentic commerce ecosystem matures. Engineering teams should prioritize interoperability in protocol selection to preserve architectural flexibility.

- Compliance architecture, not compliance audits: Colorado’s AI Act becomes enforceable in June 2026. SOC 2 auditors are already reviewing AI agent controls. Treating compliance as a periodic review rather than a continuous architectural constraint means building to catch up permanently. Organizations that embed regulatory requirements into system design from the outset will scale agentic deployments with confidence. Those that treat compliance as a checkbox exercise will face mounting technical debt and operational friction as enforcement timelines accelerate.

Final Verdict: The Wallet Is Already in Your Architecture

Every durable advance in commercial infrastructure traces a change in what became possible to transact, between whom, and at what speed. Credit cards enabled e-commerce. SSL establishes consumer trust. One-click checkout created habitual purchasing. Each primitive did not merely accelerate existing commerce. It unlocked categories of economic activity that previously could not exist. The entities that built and owned that enabling infrastructure extracted compounding value from every transaction that followed. The protocol ecosystem around x402, ACP, UCP, and AP2 represents a contest over who defines the settlement layer of an economy that is materializing faster than most organizations have planned. Annualized transaction volume on x402 alone exceeds $600 million, less than twelve months after public launch. Institutional backing from Visa, Mastercard, AWS, Google, Stripe, Shopify, and Microsoft reflects infrastructure investment, not speculative positioning.

Engineering teams building on Bedrock, OpenAI, and Google commerce stacks will have deployment models that increasingly carry financial capability. Organizations that deliberate carefully about what that means for the organization, people, and build governance infrastructure around their vision and capabilities will capture the resulting value.

Your AI will need a wallet because economically autonomous agents cannot function without a financial identity. The digital wallet provides a secure identity layer that makes autonomous commerce technically feasible and financially accountable. AI agents already research, book, negotiate, and decide. The ability to resolve business transactions and remuneration is a milestone that unlocks end-to-end autonomy.

The infrastructure to enable financial capability is already shipping from major cloud providers, payment processors, and protocol consortia. The wallet your AI carries is already part of your architecture. The imperative decision remaining includes what you are authorizing the AI agent to do, defining guardrails to protect your organization, an approach to embed new processes into work culture, and how business strategies will evolve with AI commerce in the future.